A no-fluff breakdown of the five cards actually worth carrying this year, whether you're a frequent flyer, a grocery spender, or someone who just wants their money to work harder.

Published February 2026 | Updated based on 2025–2026 card refreshes

I have spent the last several years obsessively comparing credit card benefits, opening and closing accounts, and tracking rewards value to the last cent. What I keep telling people is this: the best card is not the most advertised one. It is the one that aligns with how you actually live. This guide cuts through the noise.

The US credit card market in 2026 is genuinely competitive, but it is also noisier than ever. Between $895 annual fees, increasingly complex statement credits, and rewards that quietly erode in value, choosing wrong costs real money. I put this guide together to help you make a smarter call, whether you travel constantly or just want a reliable card for everyday spending.

The five cards below were selected based on real-world return on spending, ease of benefit use, and total annual value after fees. No card on this list made the cut for marketing reasons alone.

Quick question before we dive in: Are you primarily optimizing for travel rewards, cash back simplicity, or premium perks? Your answer changes everything about which card earns a permanent spot in your wallet.

The 5 Best US Credit Cards of 2026

Card 01 of 05

Chase Sapphire Preferred

Best All-Round Travel Card Under $100 Annual Fee: $95

If there is one card that has earned its reputation through consistency rather than hype, it is the Chase Sapphire Preferred. The Points Guy named it the best all-round travel card for a record-setting eighth year in a row in 2026, and having used it as a daily driver for travel spending, I understand why.

- 5x points on travel booked through Chase Travel, 3x on dining, streaming and online groceries

- Up to $50 in annual hotel credits through Chase Travel

- 10% anniversary points bonus on total prior-year purchases

- Primary rental car insurance, trip cancellation/interruption coverage

- 14+ transfer partners including Hyatt, United, and Air France-KLM

- Complimentary DashPass through December 2027

My Take: The 10% anniversary bonus is easy to overlook but genuinely valuable. Spend $20,000 in a year and you receive 2,000 extra points on your anniversary — essentially a quiet loyalty reward that compounds over time. The sweet spot here is using Ultimate Rewards points to transfer to Hyatt, where you can extract 2 cents per point or more. That math makes a $95 annual fee look almost laughably reasonable.

Card 02 of 05

American Express Platinum Card

Best for Premium Travel Perks & Lounge Access Annual Fee: $895

Yes, $895 is an uncomfortable number to type. But the 2025 refresh of the Amex Platinum was notably better executed than its competitors', with benefits made available to existing cardholders immediately upon announcement — something that sounds basic but proved to be a meaningful differentiator. That transparency earned it the top premium card spot at the 2026 TPG Awards.

The honest truth about this card: it only makes sense if you can use the credits. If you travel five or more times a year, the math works. If you don't, it doesn't, and no amount of marketing gloss changes that.

- 5x Membership Rewards points on flights booked direct and through Amex Travel (up to $500,000 annually)

- Access to 1,550+ airport lounges globally, including Centurion Lounges and Priority Pass Select

- $200 annual Uber Cash ($15/month + $20 bonus in December)

- $200 hotel credit via Fine Hotels + Resorts collection

- $120 in Uber One credits annually

- Global Entry or TSA PreCheck credit ($120 value)

- Elite status fast-tracks at Marriott Bonvoy and Hilton Honors

My Take: I once made the mistake of applying for this card without a clear plan to use the credits. The lounge access alone did not justify it for someone who flies ten times a year domestically. The Platinum card rewards people who travel internationally, use Uber regularly, and stay at premium hotels. If that is your life, this card essentially pays for itself. If it is not, the Sapphire Preferred will serve you better at a tenth of the cost.

Card 03 of 05

Capital One Venture X

Best Premium Card for Simple, Flexible Redemptions Annual Fee: $395

The Venture X has become one of the most compelling cards on the market by doing something unusual: offering premium perks at a mid-range price, while keeping redemption genuinely simple. You earn 2x miles on everything, with higher rates on travel booked through Capital One. But the real reason people love this card is that you can use miles to erase any travel purchase, no transfer gymnastics required.

- 2x miles on all purchases, 5x on hotels and rental cars via Capital One Travel

- $300 annual travel credit (easy to use, no enrollment required)

- 10,000 bonus miles on each account anniversary (~$100 value)

- Priority Pass lounge access for cardholder and up to two guests

- Transfer to 15+ travel loyalty programs including Air Canada Aeroplan and Turkish Airlines

- $120 Global Entry or TSA PreCheck credit

- No foreign transaction fees

My Take: The $300 travel credit is legitimately easy to use — it applies broadly across travel purchases without requiring you to book through a specific portal. When you factor in the 10,000 anniversary miles and the credit, the effective annual cost of this card is closer to zero for anyone who travels at all. The TPG Awards recognized it as the best value premium card in 2026, and I think that assessment is fair.

Expert Insight

One thing most card guides underemphasize: the value of a card's transfer partners changes over time. In 2026, Capital One added Turkish Airlines as a transfer partner, which quietly opened up some of the best award redemption opportunities available on Star Alliance flights. If you are willing to learn one transfer trick, moving Venture X miles to Turkish for Star Alliance partners can deliver outsized value on premium cabin bookings.

Card 04 of 05

American Express Gold Card

Best for Foodies and Grocery Spenders Annual Fee: $325

If your biggest spending categories are restaurants and supermarkets, the Amex Gold is genuinely hard to beat. The earning rates on dining are some of the highest available on any card right now, and the annual credits are structured around spending categories that most people use naturally.

- 4x Membership Rewards points at restaurants worldwide

- 4x points at US supermarkets (up to $25,000/year)

- Over $400 in annual credits through dining and rideshare benefits

- $120 annual dining credit (Grubhub, The Cheesecake Factory, and select partners)

- $120 Uber Cash annual credit for Uber Eats and rides

- No foreign transaction fees

- Full access to Amex's transfer partner network (Air France-KLM, Marriott, Hilton, and more)

My Take: The annual credits technically offset most of the annual fee, but only if you actually use Grubhub and Uber. The one error I see people make repeatedly is applying for this card, not adjusting their habits to capture the credits, and then wondering why it feels expensive. If you already order food delivery and use rideshares, this card is an easy win. If neither habit applies to you, look elsewhere.

Card 05 of 05

Wells Fargo Active Cash Card

Best No-Annual-Fee Card for Everyday Simplicity Annual Fee: $0

Not everyone wants a rewards strategy. Some people want a card that works perfectly and costs nothing to hold. The Wells Fargo Active Cash has quietly become the top recommendation for that use case in 2026. It earns a flat 2% cash back on every purchase, with no rotating categories, no quarterly enrollment, and no complicated redemption process.

- Unlimited 2% cash back on all purchases, no exceptions

- $200 cash rewards welcome bonus after $500 in spending within three months

- 0% intro APR for 12 months on purchases and qualifying balance transfers

- Up to $600 in cell phone protection when you pay your bill with the card

- Visa Signature benefits including rental car coverage and 24/7 concierge

- Flexible redemptions via statement credit, direct deposit, or ATM cash

My Take: The 2% flat rate at no annual fee is genuinely the highest available on a no-fee card right now. For someone who spends $3,000 a month, that is $720 a year in cash back, completely automatically. The cell phone protection benefit is also underrated — losing or damaging a $1,200 smartphone hurts significantly less when you have up to $600 in coverage built into a card you are already using.

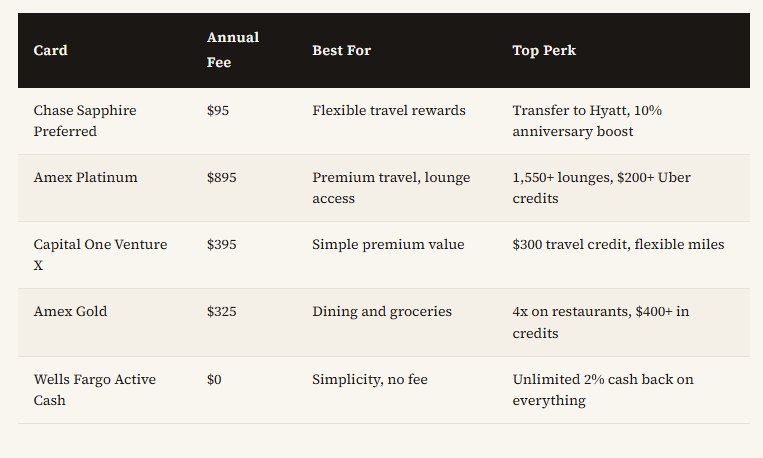

Side-by-Side Comparison: Which Card Wins for You?

The Mistake Most People Make When Choosing a Card

The most common error is optimizing for the welcome bonus rather than the long-term earning structure. A 75,000-point sign-up bonus sounds exciting, but if the card earns 1x on your actual spending categories for the next three years, you will end up worse off than someone who chose a card with 2-3x on categories they actually use.

The second mistake is ignoring how hard the benefits are to use. A $300 travel credit that requires booking through a specific portal, activating quarterly, and meeting minimum thresholds is worth less than a $200 credit that applies automatically to any purchase coded as travel. Always ask: how many steps does it take to capture this benefit?

Here is something worth thinking about: How much did you spend on dining out, travel, and groceries last year? Run the numbers using the earning rates above. The card that looks most impressive in the brochure is not always the one that returns the most cash to your pocket.

What to Expect from Credit Cards Through the Rest of 2026

The premium card market is bifurcating. At the top end, issuers are continuing to raise annual fees and pile on statement credits that require active management to extract value from. At the middle tier, cards like the Venture X are proving that you can offer premium-adjacent benefits without the complexity.

One trend worth watching: experiential perks. Several issuers are investing in benefits tied to concerts, sporting events, and exclusive dining experiences rather than pure point multipliers. Whether that appeals to you depends entirely on your lifestyle, but it signals a shift in how card companies think about differentiation beyond the rewards rate.

Also worth noting: the regulatory environment around interchange fees continues to evolve. Some issuers have quietly restructured their rewards programs in anticipation. The cards on this list have all maintained strong value propositions through recent changes, which is part of why they made the cut.

There Is No Universal Best Card

After years of testing credit cards and watching the market shift, the honest answer is that the best card depends entirely on your habits. The Chase Sapphire Preferred remains the safest default for most people. The Venture X is the best value at the premium tier. The Active Cash is the best card if you want to stop thinking about credit cards entirely.

The most important thing is that you have a card working for you rather than against you. Even modest rewards optimization on everyday spending can return several hundred dollars a year that would otherwise go unearned.

One last thought: cards change. Annual fees get adjusted, benefits evolve, and what is best today may shift by mid-year. Always check the current terms directly with the issuer before applying.

Sam Smith

Related Posts

OpenAI Plans Aggressive Workforce Expansion to Nearly 8,000 Employees by End of 2026

Read moreMeta Weighs Major Workforce Reduction Amid Surging AI Infrastructure Costs

Read moreRobinhood Launches the Platinum Card: A Premium Entry into the High-End Credit Card Market

Read more